Wall Street Insider Reveals:

The Little-Known “Banking

Loophole” That Could Net You Up To 28.99% Interest on Your Money

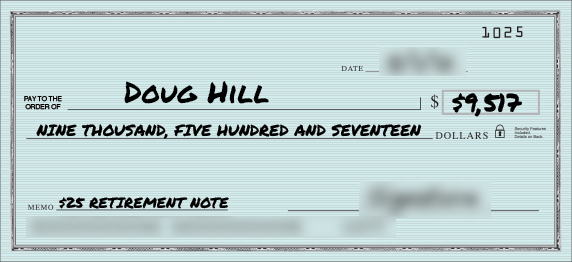

Wall Street has been trying to keep these PROVEN monthly paychecks — as high as $9,517 — for themselves.

But everyday folks are catching on…

and you could be one of them.

Dear Reader,

I recently heard something that absolutely shocked and outraged me.

In 2006, a little-known ex-Wall Street banker discovered a crazy "loophole" in a "banking system" designed to do one thing:

Enable investors to earn an incredibly high income on their money—for years—via regular monthly paychecks.

The returns on this investment can be staggering…

-

3,121% more than what U.S. savings bonds have recently returned…

-

12,727% more than the average return on a Certificate of Deposit…

-

And a whopping 48,216% more than your average savings deposit return…

When I first heard about these incredible returns, I was getting around 0.06% interest on my savings account.

At the end of a year… I’d have maybe $19 in interest if I was lucky.

“Why even bother!” I thought.

So when some well-connected investor friends told me about this new kind of investment… I admit I was curious.

To my astonishment, they were getting monthly paychecks in the mail for as high as $9,517.

I was always told that the kind of money people were making just didn’t seem possible without risking it all in the stock market.

Getting close to retirement myself… my appetite for risky bets is dwindling.

But I want REAL returns on my money… the kind we used to get 20 years ago.

So I launched a full investigation into this strange and lucrative new income source.

I found hundreds of other Americans who collect more income than they ever dreamed:

-

People like Bill L., in Houston. Before discovering this investment, he was collecting only $17.16 in interest per year from his savings account. And his retirement looked bleak.

To his amazement, after just over 4 months he had received $579.23 in interest. That’s 34 times MORE than he was collecting from his savings account. And it only took four months.

Bill was literally blown away by his success: “Damn, that is somereal moneypouring in from that relatively small amount of principal,” he said. “Returns at 20% are much higher than predicted.”

-

There’s Greg J., an investor who said, “With an annualized return over 17% to date, I am very pleased with the results so far. This is a valid way to earn higher returns in today’s low-yield environment.”

-

And Robert L. of Auburn, California. After starting with just $500, he watched in amazement as his average returns came in at a whopping 19.18%. Last I heard, he was making so much money that he’s already making big plans for the future and is buying a second home.

As I dug further into this incredible idea… something was nagging at me.

Were these people the lucky few… or was this a real solution that anyone could use?

I was determined to find out.

So I asked my good friend, Mike M., from Florida.

His results were so incredible that after I heard his story, I had to call him.

I wanted to make sure this opportunity was real.

During our call, Mike told me he heard about this investment through his connections on Wall Street.

Intrigued, he started investing in November 2013.

And the cash started pouring in almost immediately.

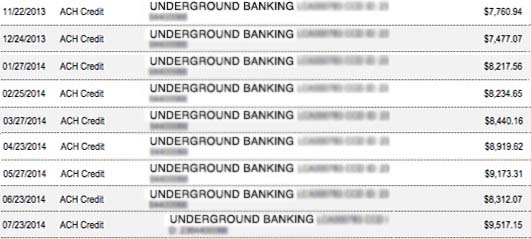

He even shared his bank statement with me. Check it out…

As you can see, Mike was getting thousands of dollars every month… like clockwork.

That’s a return of more than $76,000 in just nine months.

Of course, like any other investment, there are risks involved—and the more you invest the more you stand to make. There are no guarantees you will never lose money.

But as you already saw—I found hundreds of other Americans who are collecting more income than they ever dreamed.

Seeing these incredible results for myself I wondered…

“Why Have I Never Heard About This Before?”

Mike directed me to a strange website I’d never heard of.

And there I found something astonishing.

This source of income is completely outside the U.S. banking system…

As I found Bloomberg reported, this opportunity is only available “outside of conventional banking.”

In other words, this has nothing to do with traditional sources of income, such as dividend stocks, bonds, CDs or savings accounts.

What I really love about this incredible income loophole is that you can get started with just $25.

So you don’t need to be incredibly wealthy.

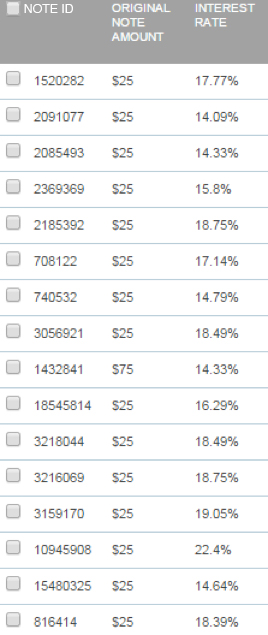

When I logged into this website…

To my surprise, I found thousands of these strange high-yielding “notes.”

I found these are not stocks, bonds, options, bank CD’s, dividends or anything else I’d ever heard of…

These notes are something entirely different that has only existed for a few short years.

Check out this screenshot from my computer…

As you can see, the notes have two things in common:

-

They only cost $25 each…

-

They pay a super high interest rate… in many cases 107 times higher than what bank CDs are paying.

And you can buy as many or as few of them as you want.

I found that if you buy enough of these things—and the right ones—you could add as much as $9,517 per month to your retirement income… almost effortlessly.

That’s an extra $110,000 per year… more than twice what the average American household earns.

I’m sure I don’t have to tell you… that can lead to an incredibly comfortable retirement.

That’s why I started calling them “$25 retirement notes.”

So at this point in my research… I knew I had to buy a few and see if these strange notes could work for me.

I bought up just a few of these notes to experiment with just a couple thousand dollars…

After all I’m not some rich Wall Street guy and I’m not going to take crazy chances with my own retirement…

And I can tell you after two years of this experiment… I’m earning extras as much as $199 a month almost effortlessly.

My name, by the way, is Doug Hill.

I’m not a broker.

I don’t work on Wall Street.

Instead, I’ve made it my life’s work to show every American how to live a happy, healthy, and wealthy life… using 100%-legal strategies to lower your tax bill, reclaim your online privacy, receive better health care, and save and grow your wealth.

I am publisher of an independent newsletter called the Laissez Faire Letter, which I’ve built from nothing to more than 112,000 subscribers.

When we discovered this incredible wealth-generating opportunity, we immediately told our readers to jump on this idea. Many of them did…

And the results were fascinating…

Reader Ellis M. said:

"Initially I put in $5,000. Then when I saw how it was making me money, I added another $10,000... I set it up to have the income automatically reinvested at that point. I've made around $7,600."

Reader Daniel F. said:

"A good place to put some money to earn better returns. My account has averaged approximately 8% since opening."

And reader James D. said:

"I have made money. A lot more than the bank."

Many more readers were absolutely ecstatic about the results…

Getting steady, reliable income at these levels is almost unheard of.

So I wanted to tell you about this opportunity now.

You see, while these notes remain a secret to most everyday investors…

Wall Street elites have been quietly buying them up.

“[$25 retirement notes] is going to be the next big wave of finance…”

–John Polito, BNY Mellon]

“Hedge funds and wealth managers have been the

dominant investors [in $25 retirement notes]…”

–the Financial Times

For example, John Mack, former chairman of Morgan Stanley, has invested several million of his own capital in these notes.

When asked about it, he said:

“Three-year Treasury bonds are paying 0.4% in interest. With [these notes], you can get at least 7%. Given where interest rates are today, there’s a real opportunity here.”

Vikram Pandit, the former CEO of Citigroup, is also deeply involved. He called this phenomenon a “radical transformation of the global banking landscape.”

In fact, by some estimates Wall Street increased the number of “retirement notes” they invested in by more than thirty fold between 2013 and 2017… totaling nearly $8 billion.

And even though the payoffs can be huge…

The really groundbreaking part is that since their inception, serious investors have enjoyed 99.9% reliable returns from these notes.

You can’t get that kind of security from stocks… not by a long shot.

Of course, as with any investment opportunity, there is still an element of risk.

But after you see some of the extraordinary returns I discovered, I bet you’ll agree—the potential here is staggering.

I’m 100% convinced these notes could be the solution to baby boomers who are struggling to get retirement income.

But you don’t have to take my word for it…

Just take the next few minutes to see a few things I’ve discovered. Then decide for yourself.

A Retirement Solution Born

in the Midst of the 2008 Crisis

It’s no secret the big Wall Street banks control much of the world’s capital flow.

So when Goldman Sachs, Morgan Stanley, JPMorgan Chase, Bank of America, and Citigroup got in trouble in 2008, they all stopped lending. Credit dried up.

Since then, it has been extremely difficult and expensive for consumers to get loans from banks.

Ronald Lester, a serial entrepreneur and former Wall Street attorney, came up with an ingenious solution.

He developed a revolutionary website that connects investors directly with borrowers, cutting the banks out of the equation.

Mr. Lester had long been frustrated with the low interest rate he was getting from his bank.

He noticed the “spread” between the 1.5% interest on earnings from his “high yield” certificate of deposit and the massive 18% rate his credit card company was charging him may have been great for greedy lenders… but terrible for consumers like you and me.

He realized that removing the banks from the equation would allow everyday Americans to collect much higher interest.

Since then $25 “retirement notes” have been growing steadily in popularity.

When you buy a “retirement note,” you’re essentially providing funds to someone who is looking for credit.

Consumers asking for loans are put through a rigorous credit-verification process… income, credit-worthiness and dozens of other factors are taken into account and bad credit risks are screened out before you ever lend money.

In exchange, you have the potential to collect a very high yield… as high as 28.99%.

This allows everyday investors to literally “become the bank”… but without all the regulatory hassles and capital requirements that real banks have to put up with.

And because you don’t have to loan out the entire amount… you can buy a fraction for as little as $25… you can spread the risk among thousands of notes so it’s much safer.

In fact, as I was researching, I came to realize three crucial points about this incredible breakthrough:

-

#1. This market’s average returns have been growing consistently since the beginning. The average annual return has been growing from roughly 7% in 2009 to nearly 10% in 2014… and if returns so far this year have been any indication… even better days are coming.

-

#2. This market has been roughly doubling in size every year… it hit $22 billion in 2016. Morgan Stanley proclaimed it could grow as big as $490 billion by 2020.

That means ever-increasing wealth-building opportunities for you… a safer retirement and a better life.

-

#3. This is a perfect opportunity for retirees or those near retirement. What this really can do is produce a steady stream of reliable income for you and your family every single month.

So, you can reap the benefits now and “pay yourself” immediately from your monthly earnings… or reinvest them for even bigger gains. You have complete control.

And if you’re concerned about the risks involved with this kind of opportunity, you needn’t be.

During my investigation I discovered that…

Virtually EVERYONE Has Made

Money With These Notes

Sure, like any other investment, these notes carry certain risks.

But what I discovered on this little-known website is their own research shows that by following a simple “protocol,” 99.9% of investors who invested in these notes have made money.

Even the Wall Street Journal acknowledged that fact:

“For income investors, ["$25 retirement notes" are] better than recent corporate-bond returns. And a 99.9% chance of making money is better than you’ll get from any IPO.”

You can’t get that kind of security from stocks, options, or mutual funds.

And you can’t get these big returns from bonds, money market funds or CDs.

This is really the best of both worlds: high returns with low risk.

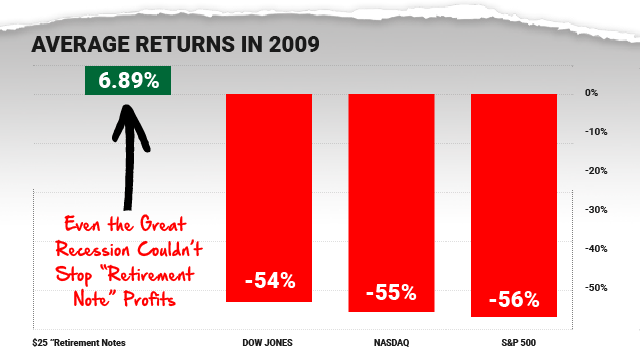

Even more amazing… the income from these notes is so reliable that investors saw healthy returns even during the last stock market crash.

Check this out:

Not only are these returns very real… they are even crash-proof.

How is that possible?

These notes are immune to stock market crashes because they don’t have any exposure to stocks.

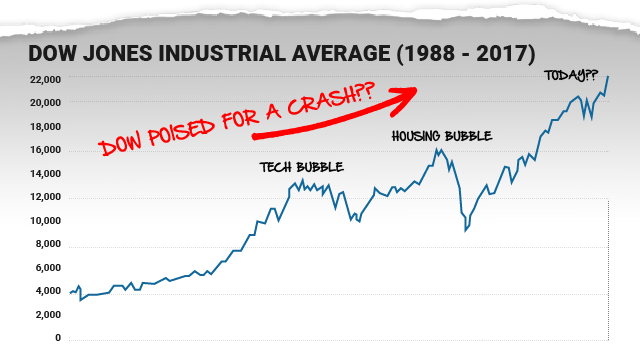

This is especially important today because another market crash could be just around the corner.

See for yourself:

If you’re like me… you are still feeling the sting of the 2008 crash.

I know I don’t ever want to go back to those days… feeling your heart sink as you watch stocks tumble day after horrible day.

Watching your portfolio get slashed in half… and wondering if you’ll even have a retirement.

When you’re in the stock market you just have to put up with the threat of collapse.

But with $25 “retirement notes,” you don’t have the risk of losing half of your money suddenly due to a crash.

That’s part of what makes them a great retirement nest egg. That explains why…

Americans Are Moving Billions Into These Notes

Instead of collecting 0% from their savings accounts, more and more Americans are moving their cash into $25 “retirement notes.”

Take a look…

Could that explain why Wall Street's cronies at the SEC temporarily shut down these notes a few years ago?

Or is this just a big coincidence?

I’ll let you be the judge.

All I know is that Americans have moved more than $22.6 billion into these notes.

And I can’t blame them…

Why would you keep collecting 0% from your bank account, if you can get up to 28.99% from these notes?

And don’t even bother asking a broker about these notes.

The Only Way to Buy These Notes

You can’t buy these notes from Ameritrade, E-trade or any other brokerage account.

Instead, you can only access them through a few little-known websites.

Now, the particular website I’m recommending isn’t some shady website run by some kid in his mom’s basement.

Some of the smartest people in finance and Silicon Valley are behind this website.

People like economist Lawrence Summers, President Emeritus of Harvard University… and Hank Morrison, former president of Visa Inc….

Former PIMCO CIO Mohamed el Erian holds a $12 million stake in this webste.

And even internet giant Google has invested $125 million.

So you can be certain this is a safe online platform.

And once you log in (I’ll show you how in a moment), you’ll have the chance to boost your income by thousands of dollars a month.

Gains for some investors have been mind-blowing, even to a veteran investor like me:

-

Mark F. saw gains of $53,539 over 6 months

-

Carl P., saw a gain of $67,419 over 14 months

-

Isadore P. saw gains of $226,080 over just 4 months

-

And Walter B. saw a whopping $1.39 million in gains over just 6 months.

Of course, the more notes you buy, the more money you can make… bigger gains require bigger stakes.

But as you can see, impressive gains are definitely possible. Instead of collecting 3% from dividends or corporate bonds… 2% from a government bond… or 0.06% from savings accounts…

You will have the opportunity to collect returns as high as 28.99%...

Instead of losing sleep at night, worrying if you’ll ever have enough to retire comfortably…

You’ll finally be able to start planning that vacation you dreamed of…

Build that addition to your home you’ve always talked about…

Or even sail around the world in your new forty-foot sailboat.

How to Grow Your Money Even Quicker

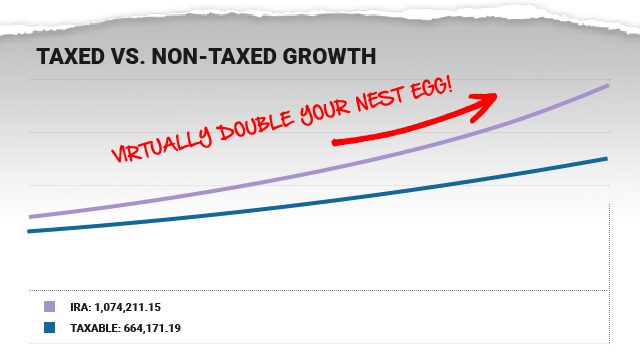

You can even take those notes and stick them in a special “self-directed” IRA and reap the tax benefits.

Over time… that could turbo-boost your returns in a big way.

Assuming a conservative annual return of 10%, this tax-saving strategy could add an extra $406,000 to your nest egg.

Wouldn’t it be nice to have that kind of extra money in retirement?

More money means greater assurances… better health, better living, more vacation options, and a greater legacy for your family.

And it’s incredibly easy… you can set all this up straight through the website with just a few clicks of your mouse.

As one veteran “$25 retirement note” investor said:

“Personally speaking, I enjoy saving for retirement this way. It is fun to watch my savings grow while knowing I will withdraw them tax-free when I turn 65… my [‘$25 retirement note’] IRA is a delightfully boring thing to maintain.”

There’s Just One Catch: Not Everyone Will Get In

If you are really serious about discovering how to become one of the 99.9% of investors that realized positive returns…

And ensuring yourself a more reliable retirement income away from the choppy waters of the stock market…

You’ll want to buy into this as soon as possible.

See, these notes are not like shares of a company that are issued by the millions.

There are a very limited number of them available in the market.

In fact, I noticed that this website I’ve been telling you about only had 190,260 notes available.

And institutional investors are already grabbing every note they can.

Major hedge funds Arcadia Funds, Ranger Capital Group and Santander Consumer USA have bought up millions of dollars’ worth of notes, according to the New York Times.

HCG Funds, Colchis Capital, Eaglewood Capital, and Disruption Credit have collectively invested more than $300 million.

Why? Because as one Wall Street investor noted, this isn’t just a hot new stock: “This is without doubt an emerging asset class.”

Former Treasury secretary and famed economist Larry Summers even said this new asset class has “the opportunity to transform finance over the next generation.”

I’m not exaggerating when I say that soon everyone is going to hear about it.

If you don’t act now, you may be left out of this incredible opportunity.

Don’t wait and regret it later.

The secret is already starting to leak into the mainstream media.CNBC recently noted investors were attracted to what I call “$25 retirement notes” by what it called “juicy returns.”

Bloomberg financial news proclaimed: “No one is scoffing at [$25 retirement notes] anymore… It’s easy to see why investors are so enthusiastic…”

And the Wall Street Journal commented recently on the incredible buzz in the financial industry these notes have been causing:

The main driver, the investors say: higher returns. Ultrasafe five-year U.S. Treasurys yield just 0.9%, while, at the other end of the risk spectrum, U.S. high-yield corporate bonds have yields of 7.33%. By contrast, [$25 retirement notes], pay a 10% average annual interest rate…

And remember, that’s just the average. I’ve easily found notes that pay more than 28% annualized.

Even better… getting started couldn’t be easier.

Follow These Three Easy Steps to Get Started Today

To get you started today, I put all the details you’ll need to know in a special beginner’s guide.

It’s called: The $25 Retirement Income Plan.

This guide will reveal everything you need to know. For example:

-

How to get started in 30 seconds with just 4 clicks of your mouse.

-

How to best use “filters” to find the best notes and the chance to max out your returns.

-

How to “set it and forget it” and collect monthly checks anywhere from $450 to as high as $9,517… with almost no effort.

-

You’ll also learn how to “turbo-boost” your returns and potentially make an extra $406,000 by the time you retire.

And that’s just the beginning.

The guide will show you how to earn returns as high as 28.99% by following just three easy steps:

Step 1. Log in to the website

In your beginner’s guide, I’ll tell you exactly which of these websites I recommend, and where to go.

Now, there are certain restrictions by state that

determine whether you can open an account.

If you live in Ohio… sorry, you can’t open an account yet.

For everyone else, I’ll tell you exactly what to expect,

and how to deal with any issues that may arise.

Once you’re on the website, you'll need to set up an account.

It’s 100% free. You can get started with as little as $25.

It’s very easy and just takes a few minutes.

But just to make sure you don't run into any snags...

This guide will walk you through the entire process... step by step so there's no guesswork on your part.

I’ve also included an 800 number you can call, just in case you would rather talk to a live person.

Once your account is set up, you can move on to step 2...

Step 2. Follow the “Protocol” to become one of the 99.9% of investors enjoying positive returns

Do it right and you could start getting monthly checks like these:

Once those monthly checks start growing… you can either re-invest those profits or start using them to cover daily living expenses… your cable bill, your mortgage, or even treat yourself to eating out more.

But if you want to become one of the 99.9% of investors enjoying positive returns, you must follow the “protocol” when you buy these notes.

This is very important.

See the “protocol” tells you exactly what notes to buy to maximize your income and reduce your risk.

Not all investors know about this “protocol”… and some have been disappointed.

But you don’t have to be.

The “protocol” is what makes this new kind of income investment uniquely safer than most… in addition to practically ensuring freakishly high returns.

In fact, some research indicates that of investors who followed this “protocol” — only 0.1% of them did not enjoy positive returns.

That's a one tenth of a percent chance you will end up being one of the losers.

You won't find that kind of proven security in any other investment with this kind of return.

Your beginner’s guide will show you exactly what this "protocol" is so there is no mystery.

Then you can move on to step 3...

Step 3. Collect your monthly income checks

Once you're through the process, you will start receiving a check every month.

You can choose to create a regular account and just pocket your monthly earnings...

Or you can create a retirement account and reinvest all those earnings safely away from the taxman.

As you watch your money grow, you'll see all sorts of new options open up.

Things that you thought were unaffordable you'll find are suddenly within reach.

New house... new car... more money for that cruise you've planned or that trip to Italy...

People are living that reality through “$25 retirement notes” right now.

I think you should be one of them.

So I want to grant you immediate access to my exclusive beginner’s guide called The $25 Retirement Income Plan.

Once you learn all the details in your guide, you’ll be able to open an account and finally put your retirement back on track…

No more worrying about the stock market’s stomach-churning ups and downs…

No more lying awake at night, wondering what would happen if you were to run out of money in retirement…

That’s the kind of financial freedom these notes offer. I’ve made this beginner’s guide available for you online.

But because of the limited number of notes available, I can’t simply post this information online for everyone to see.

Right now, only readers of my monthly research advisory have access to this guide. I’ll tell you how you can get into my network in a moment.

First, let me tell you more about The Laissez Faire Letter.

Growing Your Wealth Outside Wall Street

Like I said before, my name is Doug Hill.

And I’m publisher of an organization called the Laissez Faire Club.

As you may know, “laissez faire” is a French term that means “let them be”…

The ultimate goal of the Laissez Faire Club is to show you new ways to live a healthier, wealthier and more productive life…

With more freedom from Big Government and Wall Street.

We’re big believers in self-reliance…

And in just three years, our self-empowered group has grown from essentially zero readers to 112,000 strong.

And don’t worry. We’re not some doomsday group or fringe political party.

My research team consists of top experts in their respective fields. For example, in our club we have…

-

A three-time New York Times best-selling author

-

A former CIA agent who specializes in self-protection strategies for everyday Americans

-

A private tax consultant to Capitol Hill and one of the IRS’s most successful tax negotiators, otherwise known as the “Loophole Queen”

-

A former Wall Street lawyer who advises the government in matters of financial risk

-

A famous investigative health researcher whose work has been featured in The Washington Post, Discover Magazine, Psychology Today, Parade, Reader’s Digest and Life magazine.

-

The former personal financial advisor to a Coca-Cola heiress and a major oil magnate... and more.

Every month, we publish our best ideas in The Laissez Faire Letter, showing readers how to become more self-reliant.

One of the best ways I can help you achieve financial independence is by finding unconventional ways to grow your wealth… outside Wall Street.

This “$25 retirement note” is just one of the many off-the-grid opportunities I’ve found.

At first glance, these moneymaking opportunities may even seem completely out of reach.

That's exactly what Wall Street wants you to think.

But nothing could be further from the truth. In fact, let me tell you about another opportunity…

Something I call…

The Secret Account of the 1%

Have you ever wondered how the rich continue to get richer through depressions, recessions and even stock market crashes?

For example…

After the 2008 financial disaster, one famous hedge fund manager walked away with $2.9 billion.

And a financial guru came out of the crisis $3.7 billion richer.

All while average retirees throughout America lost their life’s savings.

Added up, the wealth gap between the richest 1% and everyone else is larger than it’s been since the 1920s.

What’s their secret?

In short, I’ve found that they’ve used little-known investment opportunities time and time again to continue growing their wealth.

But here’s the thing… you don’t have to be rich to access those same types of investments.

I’d like to introduce you to what I call “The Secret Income Account of the 1%.”

It’s a collection of little-known investment opportunities the richest of the rich have been using — for centuries — to grow their wealth.

One of these opportunities returned an extraordinary 9,897% gain in 21 years.

And although most of these royal families and business tycoons were already sitting on substantial wealth…

They used this “Secret Income Account” time and time again to continue growing their wealth.

Even founding father Thomas Jefferson had his hand in the pot of one of these investment opportunities…

So did media mogul and multibillionaire Ted Turner.

They’ve all used this “Secret Income Account” to get wealthier year after year…

Through depressions. Recessions. Even market crashes like the one we saw back in 2008.

Just one of these ways has turned every $1 invested into more than $4,344 in the past.

Another one turned every $1 into nearly $10,000.

Now, I can’t guarantee these gains will happen again tomorrow.

But history has proven this account could turn the money in your wallet into an absolute fortune.

To be clear, this is not like a traditional income account...

For example, there are no physical locations or ATMs involved in this “Secret Income Account of the 1%.”

And it’s not some new type of 401(k) retirement account, IRA, life insurance policy, stock market plan or anything like that.

In fact, the “Secret Income Account of the 1%” has nothing to do with stocks, real estate, bonds, dividend-paying companies or anything else on Wall Street.

But a few savvy Americans have already begun to put this to work for them.

People like Allen, from Chicago, who says one of these investment opportunities helped pay for his children’s education.

Or John, who says:

"My [Secret Income Account], as a whole, has appreciated more than $1 million."

So how do you get started?

I’ve put together all my findings on the entire “Secret Income Account of the 1%” into an urgent special report I want to send you immediately.

It’s called The Secret Income Account of the 1%: Six Ways to Grow Rich Through Booms and Busts.

You’ll get access to both this report andThe $25 Retirement Income Plan for FREE…

Once you take a risk-free trial to our monthly publication The Laissez Faire Letter.

As a member, I’m confident you’ll have an easier, better retirement — all outside the traditional rigged Wall Street game.

But don't take my word for it.

Here's What Some of My Readers Are Saying

"I truly feel your genuine passion to help us investors waylaid by brokers, Wall Street and Uncle Sam. Your insight is not only appreciated, but also lifesaving financially."

—Dr. Walter T.

"What a great job you are doing to bring us readers different opportunities that are off the radar for most, if not all newsletters. Keep up the good work so we can have another profitable year ahead."

—Phil M.

"I really enjoy your service and have been doing great. Keep up the great work!"

—Steve B.

"I just wanted you to know that the $2,000 gain in one week on one position more than paid for my subscription."

—Sarah Cofax

And that’s just a small sample of hundreds of notes I receive from my readers who are already taking advantage of these off-Wall Street opportunities.

OK, by now you’re probably wondering, “How much will all this cost me?”

Before I answer that, consider this…

With the right “$25 retirement notes,” you could add as much as $9,517 per month to your retirement income.

For that reason, I could probably charge $1,000 or more for my research.

But don't worry...

A year's subscription will cost youfarless than that.

I’ll give you all the details in a moment.

First, I’d like to tell you about another incredible opportunity I found outside Wall Street.

I call it the “The Queen’s Account”

An “Account” That Has Gone up

Every Year for the Past 40 Years

Just a few meters from the English Channel in a house that Henry VIII built lies a shocking fortune.

It’s not the crown jewels, has nothing to do with gold or silver, and can’t be traded on the stock market.

Instead, I’m referring to something safer, more lucrative, and far more private.

I doubt 1 in 1000 of your friends has ever heard of it.

Inherited by Queen Elizabeth in 1952, I’ve nicknamed it the “Queen’s Account” because for the past 15 years the strategy behind it has outperformed every major market…

Even better, you don’t have to be royalty to benefit from this asset class.

Let me start with the story of Bryan Gould, a 63-year-old Californian who just got sick of the market's roller-coaster ride.

He knew there had to be another way to make steady gains... without all of the ups and downs.

That's when he discovered what I like to call the “Queen’s Account.”

Despite more than 30 successful years in the investing business, Bryan had never heard of this unique alternative to stocks.

But as he investigated further, he was amazed at the obscure “Queen’s Account” history of steady gains.

Between 1950 and 2010, some “Queen’s Accounts” had never earned less than 5% in any year.

And since 1991 — while the U.S. economy trudged through two recessions — “Queen’s Accounts” made an average compound return of 13.4% per year.

That’s enough to turn a $100,000 retirement account into more than $351,000 in just a decade.

So Bryan took a chance and moved a portion of his money into a "Queen’s Account.”

Boy, was he happy he did...

Even while the stock market crashed twice in a nine-year period, Bryan's "Queen’s Account" gained over 264%.

And this wasn’t an isolated case.

Nate Soderberg, a 47-year-old English mechanic, also invested in a “Queen’s Account.”

And he’s happy to report his account has returned between “8% and 12% every year.”

In a recent two-year span alone, his “Queen’s Account” went up 133%.

Here’s what he has to say…

Imagine an investment that has increased in value for 40 years straight... but has the potential to double your money in just two.

That's the “Queen’s Account.”

And there's nothing like it on the stock market.

In fact, during the 2008–2009 financial crisis, the value of some "Queen’s Accounts" rose a smoldering 32%.

So where do you sign up for a “Queen’s Account"?

Don't call up a broker, that's for sure.

This isn’t what you would call a "mainstream investment." Regular stockbrokers aren't authorized to trade it.

That’s because “Queen’s Accounts” have nothing to do with the stock market.

And they have nothing to do with gold, diamonds or any other conventional “hard assets” either.

But if you know where to look, it’s extremely easy to open this special "Queen’s Account."

I've created an instruction guide for beginners, called Building Wealth with the Queen’s Account.

Inside, I'll explain everything you need to know and walk you through the sign-up process, step by step.

You could start earning a hassle-free 12% per year without all of the negatives of the stock market… just like Bryan and Nate.

Some years, you might make even more.

You’ll gain instant access to this report and all the other reports I’ve mentioned today as soon as you join The Laissez Faire Letter.

Normally, a membership to Laissez Faire Letter has a list price of $99 for 12 months...

We’re able to offer such great value because we divide our costs across thousands of subscribers all over the world.

But if you subscribe today, I'll give you an even better deal. Here’s what I propose…

Take a Full Year to Try It — No Pressure

I know that in order for me to earn your trust and your business, I need to deliver on everything that I’ve promised.

For that reason, I want to make it as easy and hassle-free as possible for you to try my work today.

I don’t want price to be an issue. Which is why I asked my publisher to knock off $50 from the regular price.

I want to make this low enough for you to try, while still making it a breakeven proposition for us.

That means a full year's subscription of Laissez Faire Letter will cost only $49 if you order today.

We also want you to be 100% satisfied with your membership.

When you sign up for The Laissez Faire Letter, we'll give you a full year to test out the service — at no risk to you.

If, during those first 12 months, you find you're not satisfied with The Laissez Faire Letter for any reason at all, you can simply call or e-mail our customer service team and cancel your subscription.

We'll give you a full refund, no questions asked.

And we'll let you keep everything you receive during your year as a subscriber — at no charge.

This means there’s no risk to you at all.

It's our way of saying thank you for giving The Laissez Faire Letter a try.

Here’s everything you get when you agree to try a risk-free membership:

- 12 issues of The Laissez Faire Letter. Every month I’ll show you the best opportunities to grow your wealth outside Wall Street.

- Free Beginner’s Guide: The $25 Retirement Income Plan

- Free Report: The Secret Income Account of the 1%

- Free Report: Building Wealth with the Queen’s Account

- Private Access to Members-Only Website. It gives you access to updates, special investment research articles and unlimited access to all of our special report archives.

I sincerely hope you join us today and start getting access to all the ways you can get rich outside the stock market.

And make sure you read your report on “$25 retirement notes” immediately.

Remember, this is the only type of account in the world that offers an annual average of 10% returns and claims 99.9% of investors enjoy positive returns… but you must act soon.

There’s just a limited number of notes available.

Don’t Waste Any Time… Buy Your First $25 Retirement Note Today

Keep in mind, the Fed hasn’t let interest rates budge for the last ten years. They’re unlikely to raise them by a whole lot in the foreseeable future.

This means that you likely can’t expect any real returns from your savings account, CDs or other safe havens.

What you’ll need to retire comfortably are REAL returns on your savings… without the dangerous volatility of the stock market.

And that’s exactly what $25 “retirement notes” can offer: DEPENDABLE MONTHLY INCOME.

Look… you can either keep collecting a pittance from your bank account for years to come…

Or pocket up to 28.99% annualized returns in paychecks you receive month after month.

The choice is yours.

If you pass on this opportunity, you may be condemning yourself to surviving on a meager $1,200 monthly check from Social Security.

You don’t have to settle for that.

Imagine watching checks as high as $9,517 hitting your bank account… month after month after month.

Take action now.

Believe me… when your retirement comes, you won’t regret it.

I’m confident signing up to get our research will be one of the best financial moves you’ll ever make.

So please... don’t wait any longer to begin securing an income stream for the rest of your life.

To get started, simply click on the link below and you’ll be taken to a secure order form.

I hope you don’t miss this opportunity to secure a safe source of monthly retirement income.

Sincerely,

Doug Hill Publisher, The Laissez Faire Letter

October 2017